When it comes to financial planning, the age-old debate between life insurance and investment plans continues to puzzle millions of Indians. Should you prioritize protecting your family’s financial future or focus on building wealth for tomorrow? This dilemma becomes even more challenging when you’re working with a limited budget and can’t afford both options simultaneously.

The truth is, both life insurance and investment plans serve crucial but different purposes in your financial portfolio. Life insurance acts as a financial safety net, ensuring your loved ones remain financially secure even in your absence. Meanwhile, investment plans focus on wealth accumulation and beating inflation to help you achieve long-term financial goals. However, the modern financial offers innovative solutions that combine both benefits, making this debate more nuanced than ever before. Understanding the key differences, benefits, and hybrid options available can help you make an informed decision that aligns with your financial objectives and family’s needs.

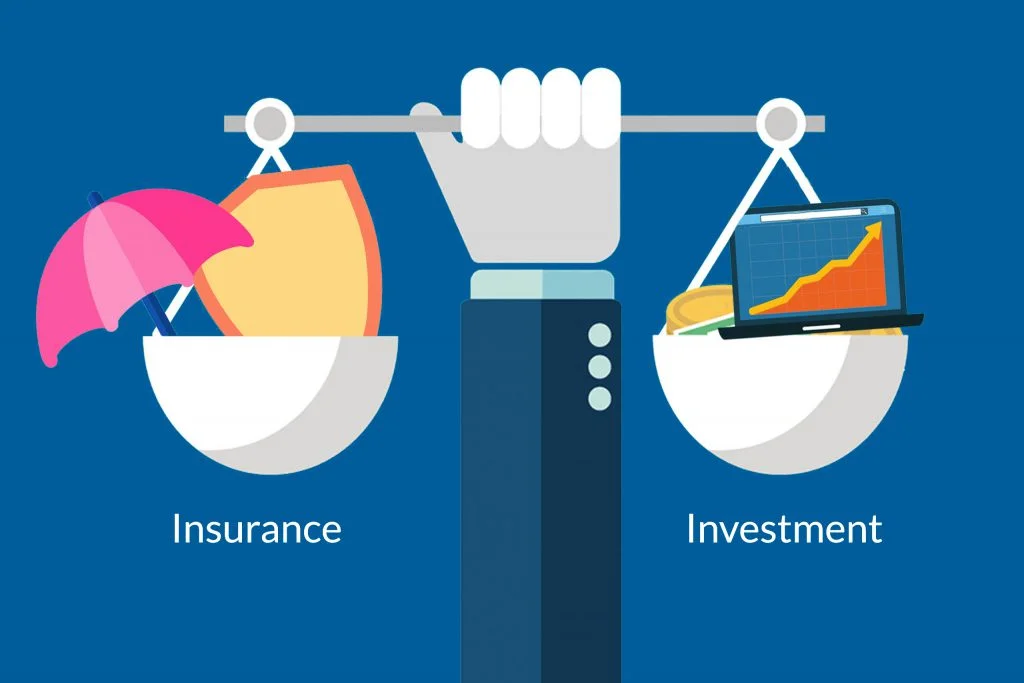

Understanding Life Insurance: Your Family’s Financial Guardian

Life insurance serves as a financial protection mechanism designed to safeguard your family’s future in case of your untimely demise. The primary objective is to provide a lump sum payout to your beneficiaries, ensuring they can maintain their standard of living and meet essential expenses.

Life insurance offers negligible risk compared to investment options, making it a stable choice for conservative investors. The death benefits are typically tax-free, providing significant tax advantages for your beneficiaries. Additionally, many policies offer creditor protection, meaning the death benefit cannot be seized to pay off debts, providing an extra layer of security.

For parents and guardians, life insurance ensures children receive financial support until they become self-sufficient. Business owners can protect against the loss of key employees, while seniors can leave a meaningful legacy for their loved ones. Even stay-at-home parents benefit from coverage, as it helps replace valuable services like childcare and household maintenance.

The predictable nature of life insurance makes it an excellent foundation for financial planning. Unlike market-dependent investments, life insurance provides guaranteed coverage regardless of economic fluctuations, offering peace of mind during uncertain times.

Investment Plans: Building Wealth for Tomorrow

Investment plans focus on wealth accumulation and helping you achieve specific financial goals through systematic investing. These plans offer opportunities to invest in various assets including equity, debt, bonds, and government securities, allowing you to diversify your portfolio based on risk tolerance.

Investment plans provide significantly higher returns compared to traditional insurance products when invested wisely. They help you beat inflation and maintain your purchasing power over time. Many investment options offer tax benefits under various sections, helping minimize your tax liability while building wealth.

The flexibility to choose from stocks, mutual funds, bonds, government schemes, and other instruments allows you to align investments with your risk appetite and financial objectives. Investment plans also enable you to earn passive income beyond your regular salary, creating multiple income streams for financial independence.

Modern investment platforms offer systematic investment plans that allow you to invest small amounts regularly, making wealth building accessible even for those with modest incomes. The power of compounding works in your favor when you start investing early and remain consistent.

The Risk-Return Trade-off

The fundamental difference lies in the risk component. Life insurance carries negligible risks but offers relatively low returns, typically including the sum assured plus occasional bonuses. Investment plans carry much higher risks but provide substantially higher returns when managed properly.

This risk-return relationship means life insurance prioritizes capital protection and guaranteed payouts, while investment plans focus on capital appreciation and wealth multiplication over time. Understanding your risk tolerance is crucial in determining the right balance between these two approaches.

Market volatility can significantly impact investment returns, especially in the short term. However, historically, well-diversified investment portfolios have outperformed traditional insurance products over extended periods, making them attractive for long-term wealth building.

Modern Solution: Hybrid Plans That Offer Both

Today’s financial market offers innovative solutions that combine life insurance with investment components. Unit-linked insurance Plans provide both life coverage and investment opportunities in a single product. These plans allocate your premiums between insurance coverage and investment funds, offering flexibility to switch between equity, debt, and balanced options.

Endowment plans represent another hybrid option, combining systematic savings with life coverage while providing guaranteed returns. For those nearing retirement, retirement annuity plans offer both life protection and guaranteed regular income during the golden years.

These hybrid products appeal to investors who want simplicity and prefer managing fewer financial products. However, they often come with higher charges and may not provide the best returns compared to separate pure-term insurance and dedicated investment products.

Making the Right Choice for Your Situation

The decision between life insurance and investment plans shouldn’t be viewed as an either-or choice. Both serve essential roles in comprehensive financial planning. If you’re a young professional with dependents, prioritizing term life insurance for maximum coverage at minimal cost makes sense while gradually building an investment portfolio.

For those with higher disposable income, combining pure term insurance with separate investment vehicles often provides better returns than hybrid products. However, if you prefer simplicity and want both benefits in one product, modern investment-linked insurance plans offer an excellent compromise.

Your age, income level, family responsibilities, and financial goals should guide your decision. Young professionals might prioritize investments for wealth building, while those with significant family obligations should ensure adequate life coverage first.

Consider your liquidity needs as well. Investment plans typically offer better liquidity options, allowing you to access funds when needed, while life insurance primarily benefits your beneficiaries after your demise.